Complete Paralysis: Just 1% Of US Homes Have Changed Hands In 2023, The Lowest On Record

Editors note: The media would have you think that the housing market is just fine as prices haven’t bottomed out yet. From Zerohedge

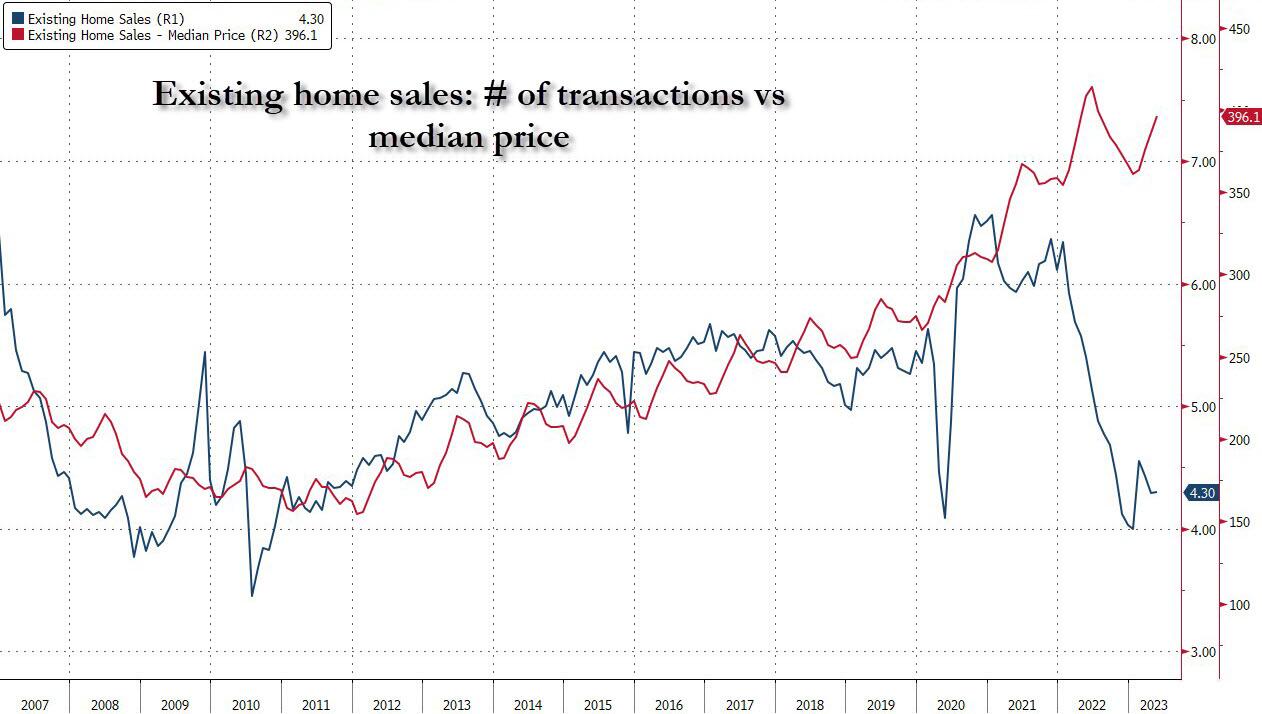

While the US housing market has remained surprisingly resilient price-wise in the face of 7% mortgage rates, which the Fed has pushed to near-Volcker levels precisely in hopes of accelerating the disinflationary wave by crushing housing, that single most valuable asset of the US middle class, the reality why prices have not collapsed is that the bid-ask spread for any home currently for sale has ballooned to levels where the market is effectively frozen as there is simply no possibility for the bid and ask to meet somewhere “in the middle” of the range (those who are hoping to buy are already tapped out before being asked to pay even more, while sellers are already wealthy and absent a liquidity crunch see no reason to sell a home at what they view as firesale prices).

Overnight, real-estate brokerage Redfin calculated just how widespread said paralysis is: it found that just 14 of every 1,000 U.S. homes changed hands during the first six months of 2023. That’s down from 19 of every 1,000 during the same period of 2019 and the lowest turnover rate in at least a decade, since Redfin’s records started. That means prospective homebuyers have 28% fewer homes to choose from than they did before the pandemic upended the U.S. housing market.

{kind=link}

Redfin uses turnover as a measure of housing availability; it indicates how often homes change hands in a given area. This analysis includes overall for-sale housing turnover and breakdowns based on neighborhood type and home type.The pre-pandemic turnover rate noted above (roughly 20 of every 1,000 sellable homes change hands in the first half of a year) is fairly typical for the modern housing market, but a more active market would have a rate closer to 40 or 50 of every 1,000.As Redfin adds, the wild pandemic-era housing market has intensified an existing shortage of homes for sale and led to this year’s low turnover rate. In 2018, Freddie Mac estimated that about 2.5 million more homes needed to be built to meet demand, with the shortfall mainly due to a lack of construction of single-family homes. The homebuying boom of late 2020 and 2021, driven by record-low mortgage rates, remote work and a surge in investor purchases, depleted already low inventory levels. Finally, 2022’s soaring mortgage rates–average rates nearly doubled from January to June–exacerbated the shortage by handcuffing homeowners to their comparatively low rates. Some homeowners have opted to renovate their current home, and some are buying another home but hanging onto their first one and renting it out to either a longterm tenant or short-term vacationers. Now, the supply of homes for sale is at a record low. Read the rest at Zerohedge.

Johnny’s notes: I remember when there was that surge in investor purchases that are mentioned in the above paragraph. Back in 2020 our landlord received some ridiculous offers for her ranch (thankfully she didn’t sell) and she said others in the area had as well. Corporations like Blackstone are buying up residential properties and either letting them sit empty and rot or they’re renting them out at much higher rates than pre-covid. Either way it created a housing shortage and drove the prices out of reach for most people, which is why the market remains stagnant.

What I see being built here in the Spokane WA area are nothing but apartment buildings. I see it even in our somewhat rural area as the older folks who owned the land for years are dying off and the relatives are selling it to developers. Those developers are ramming through plans to put up cookie cutter style townhomes and apartments to maximize their land investments. My question to them would be this…how are people going to pay $2,000-$3,000 per month in rent when incomes keep going DOWN in relation to inflation? Where are all of these rich renters going to come from?

It’s not just the housing market either, it’s the entire economy that’s crashing! In the video below you’ll see the car market and the REPOS going through the roof at levels never before seen! Brand new Teslas with 1500 miles are being repossessed! Guys if those with credit and income good enough to buy a new Tesla are giving them back to the bank the market is in HUGE trouble. That’s one market I know well as I spent almost 20 years buying, selling and financing cars.

It’s amazing to watch the world continue to make it’s plans even as God’s judgement is being pronounced all around us. “As in the days of Noah” I guess, just as Jesus said it would be in Matthew 24. They all went around making plans, getting married, giving in marriage and more until the rains came and the ground burst open! Nobody thought Noah was foolish on that day.

That’s the world we see today, everyone keeps making plans like everything will return to normal one day soon, we just need to get Trump or whoever the flavor of the week is back into office. Then everything will be fine and blah blah blah. Yep, just as in the Days of Noah…

You can support this ministry and keep us on the internet using the links below. Patreon is gone so now we have Cash App and Buy me a Coffee as our online options. The new buy me a coffee link is below.

Cash App ID: $jstorm212

Discover more from Don't Speak News

Subscribe to get the latest posts sent to your email.